In 2020, we published our inaugural Risk Factor Trends Report, which summarized the risk factor disclosure practices of the Lonergan Silicon Valley 150 (SV150) prior to the amendments to Item 105, Risk factors, of Regulation S-K (Item 105).[1] In 2021, we published the second edition of our Risk Factor Trends Report (2021 report), which summarized the risk factor disclosure practices of the SV150 following the effective date of the amendments to Item 105.[2]

The principal amendments to Item 105 include the following:

- Headings. Item 105(a) requires risk factors to be organized under relevant headings. In addition, if companies present risks that could apply generically to any company or any offering, then those risks are to be disclosed at the end of the risk factor section under the heading “General Risk Factors.”

- Summary risk factor disclosure. If the risk factor section exceeds 15 pages, then Item 105(b) requires a summary, in the form of short, concise, bulleted, or numbered statements, of the principal factors that make an investment in the company or offering speculative or risky. This summary is to be no more than two pages and is to be included in the forepart of the prospectus or annual report, as applicable.

- Disclosure standard. Item 105(a) requires a discussion of the “material” factors that make an investment in the company or offering speculative or risky. Under the previous version of Item 105, the disclosure standard was the “most significant” factors. The change in disclosure standard was intended to focus the disclosure on “the risks to which reasonable investors would attach importance in making investment or voting decisions.”[3]

Among other things, the amendments to Item 105 were intended to address the U.S. Securities and Exchange Commission’s (SEC’s) concern about the increasing length of risk factor disclosure.[4] For example, in adopting the summary risk factor disclosure requirement, the SEC stated that this requirement “may create an incentive for registrants to reduce the length of their risk factor discussion to avoid triggering the summary requirement[.]”[5]

At the time we prepared our 2021 report, only 120 SV150 companies had filed a Form 10-K under amended Item 105. Based on our review of those 120 companies, we found that both the length of risk factor disclosure and the number of risk factors disclosed had increased from the previous year.

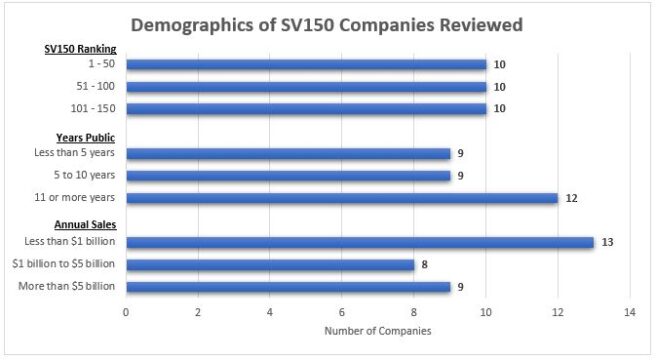

With two more years having elapsed since the amendments became effective, we wanted to provide a quick check-in on the risk factor disclosure practices of the SV150. We reviewed the risk factor disclosures in the most recently filed annual reports on Form 10-K for 30 public companies in the SV150. While this sample set is too small to summarize the results by years public, or annual sales, we selected a sample set that spanned a range of companies. The following chart reflects the demographics of the companies reviewed by rank within the SV150, number of years public, and annual sales.

Total Number of Pages of Risk Factors[6]

Based on the sample set that we reviewed, the total number of pages of risk factors appears to be continuing to increase. The average total number of pages increased from 23.7 pages in the 2021 report to 25.7 pages this year, an 8.4 percent increase. The median total number of pages increased from 23 pages in the 2021 report to 25 pages this year, an 8.7 percent increase.

Risk Factor Summary

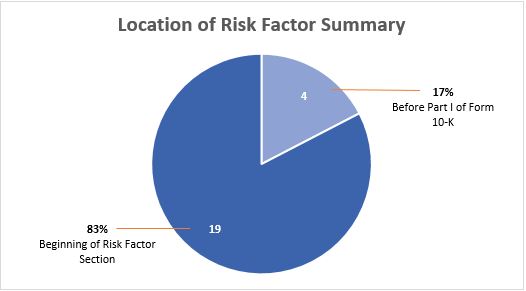

Of the 30 companies reviewed, 23 companies, or approximately 77 percent, included more than 15 pages of risk factors. All 23 companies included a risk factor summary; however, there was some variation in the location of the risk factor summary. Of the 23 companies, 19 companies, or approximately 83 percent, included the risk factor summary at the beginning of the risk factor section, and four companies, or approximately 17 percent, included the risk factor summary before Part I of the Form 10-K.

Total Number of Risk Factors

Based on the sample set that we reviewed, the total number of risk factors also appears to be continuing to increase. The average total number of risk factors increased from 48 in the 2021 report to 50.5 this year, a 5.2 percent increase. The median total number of risk factors increased from 47.5 in the 2021 report to 50.5 this year, a 6.3 percent increase.

Takeaways

Although the sample set reviewed for this Snapshot is relatively small, our review suggests that both the length of risk factor disclosure and the number of risk factors is continuing to increase.

While there are many reasons for lengthy risk factor disclosure (e.g., ensuring all material risks are adequately discussed, ensuring the risk factors are tailored to the company, liability protection), in the years since our 2021 report, several issues have arisen that may have played a role in increasing the length of risk factor disclosure including (among others) the COVID-19 pandemic and related impacts, inflation, the recent bank failures, as well as issues for which the SEC’s Division of Corporation Finance has published disclosure guidance—climate change, Russia’s invasion of Ukraine and related supply chain issues, and developments in crypto asset markets.

Our next snapshot will review the use of headings, including the “general risk factors” heading, and the quarterly report on Form 10-Q risk factor disclosure practices. Stay tuned.

[1] The Lonergan Silicon Valley 150 ranks the top 150 public companies with headquarters in Silicon Valley by annual sales. For more information on the methodology used to prepare the Lonergan Silicon Valley 150, please visit https://lonerganpartners.com/assets/pdfsdownloads/2023-LSV-150-Company-Ranking.pdf.

[2] For our 2021 report, we reviewed the risk factor disclosures of companies in the Lonergan 2020 Silicon Valley 150, which is available here (last accessed June 1, 2023).

[3] Modernization of Regulation S-K Items 101, 103, and 105, 85 Fed. Reg. at 63744 (Oct. 8, 2020).

[4] In the adopting release, the SEC stated that “[i]n proposing amendments to Item 105, we aimed to address the lengthy and generic nature of the risk factor disclosure presented by many registrants.” Id. at 63742.

[5] Id. at 63744.

[6] Similar to our 2021 report, for purposes of counting the total number of pages of risk factors in each Form 10-K filing, if no actual text of a risk factor appeared on a page, then that page did not count toward the total number of pages of risk factors. For example, if just the risk factor section heading and introductory sentence(s) were included on a page, then that page did not count toward the total number of pages of risk factors because no actual text of a risk factor appeared on that page. In addition, if the risk factor summary was included in the risk factor section, it was not counted as part of the total number of pages of risk factors. The risk factor disclosures in both the Form 10-K and Form 10-Q filings were reviewed on the SEC’s EDGAR website.